Zuora’s ® Subscribed Institute analyzed data across several quarters from over 891 companies to answer this question. For each company, we identified how much revenue was generated by new versus existing subscribers. The answer: existing subscribers (active in previous periods) generated on average 76% of a company’s annual recurring revenue (ARR), or, more generally, between 70% and 81%.

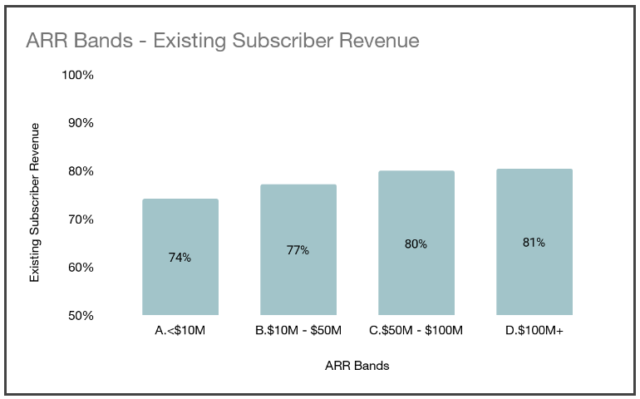

Having worked with many subscription businesses, we suspected the share of revenue generated by existing subscribers to be correlated to the degree of maturity of a business. To test this hypothesis, we classified subscription businesses into four ARR buckets: less than $10m, between $10m and $50m, between $50m and $100m, and over $100m. This analysis (see Figure 1) demonstrates that smaller subscription businesses have a lower share of their revenue generated by existing subscribers (74-77%) than more established subscription businesses (80-81%). In other words, as a company grows and builds a solid customer base, more of its future revenue will come from that customer base instead of new subscribers.

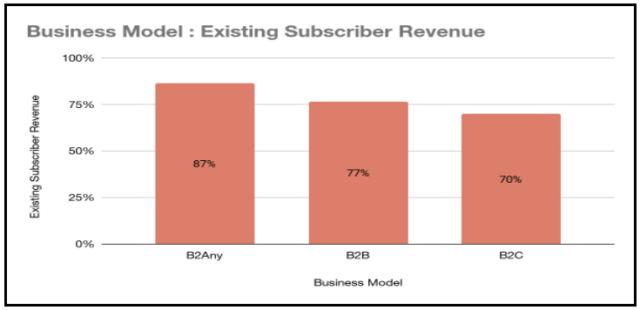

We also analyzed the differences between B2B and B2C (see Figure 2). Businesses targeting consumers tend to have a lower share of revenue generated by existing subscribers (70%) due to higher churn levels and more new subscriber acquisitions than B2B. In reverse, businesses targeting other businesses and consumers (B2Any) have 87% of their revenue sourced by existing subscribers, much higher than those solely focused on B2B (77%).

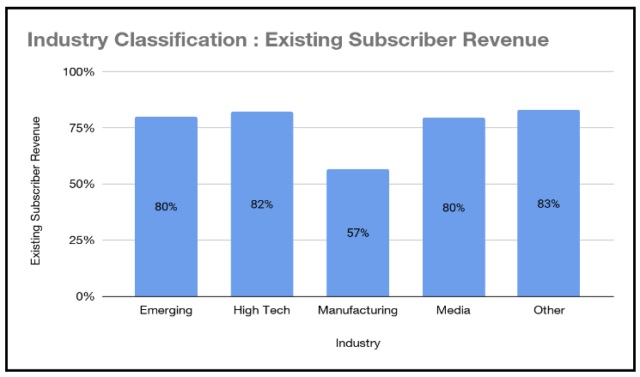

Lastly, we analyzed revenue from existing subscribers by five industry sectors (see Figure 3), and found similar revenue percentages across all sectors except for Manufacturing. In the other four industries (Emerging, High Tech, Media, and Other), existing subscribers were responsible for 80-83% of ARR (i.e., new subscribers drove 17-20%). In Manufacturing, existing subscribers only generated 57% of ARR. We attribute this relatively low share of ARR to the fact many manufacturers are in the early stages of their subscription initiatives and are highly reliant on new acquisitions for revenue growth.